Breaking down the new CARES ACT-

The US government is providing small businesses with $350 billion in loan

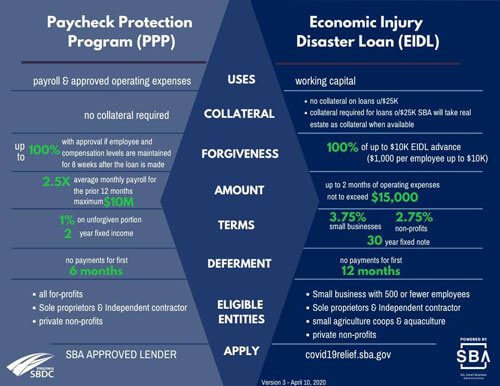

assistance to keep employees on payrolls and continue paying obligations like rent and utilities. The CARES act aims to help bridge company expenses for up to two months. Loan amounts would be forgiven if proceeds are used to cover payroll costs, rent, and utilities over the 8 week period after the loan is made and employee and compensation levels are maintained.

Tenants, Clients, and Small Business Owners:

Catch up on our collection of information below on the CARES act and Paycheck Protection Program: which can be used towards paying staff, rent, and utilities! Talk to your accounting and legal team on all your business needs and options. Tenants: feel free to reach out to your individual property manager or our dispatch line with any further questions!

Need more information on the stimulus package and what to expect? Curious how employee retention credits, and expanded unemployment bills work? Read more from our latest blog post below!

Information sourced from:

- US Chamber of Commerce

- Helpful graphics: Located here, from the US Chamber

- COVID19 federal stimulus details and business impact- webinar from US chamber of commerce and Buffalo Niagara Partnership

- Navigating the CARES act, how your small business can benefit- webinar from HSE institute

Research by Maria Owens, Esq– Senior Manager, Development and Acquisitions

Organized by Olivia Basile, Marketing Manager

What benefits are available?

- PPP forgiveness potential

- EIDL loan (no forgiveness)

- 50% employee retention tax credit

- SS tax deferral program

Loan forgiveness through Paycheck Protection Program (PPP Loans)

- Loan amount is either 2.5x the applicant’s monthly payroll costs for preceding 12 months OR 10M whichever is less.

- Payroll costs include: salaries, wages, commissions, FMLA payment, allowance to dismissal or separation (severance), health insurance premiums, retirement benefits, state/local payroll taxes, payroll costs, payments of interest on any mortgage obligations (mortgage of the borrower), rent (cannot pre-pay future rent), utilities

- Payroll Costs exclude: Salaries over 100k, taxes imposed or withheld under chapters 21,22, or 24 (FICA and Medicare), qualified sick leave or family leave for which a credit is allowed under FFCRA.

- EIDL disaster loans: apply here https://covid19relief.sba.gov/#/

- Payments on existing SBA loans

- For six months, the SBA will pay all principal, interest and fees on all existing SBA loan products, including 7(a). Borrower will not have to repay this amount.

Who benefits?

Small businesses (less than 500 employees): SBA disaster loan, paycheck protection program, paid sick leave, FMLA leave

The American people with stimulus checks: https://www.irs.gov/newsroom/economic-impact-payments-what-you-need-to-know

- Automatic Payments to Individual Taxpayers- $1,200 per individual ($2,400 joint return) + $500 per child for incomes below $75,000/year

Expanded Unemployment- Additional $600 per week on top of regular state benefit (through July 31) Changes in the labor market as a result of COVID-19: This site lists jobs in demand now- many with urgent hiring need: https://nyhirenow.usnlx.com/

- Businesses can also apply for (based on criteria): employee retention, payroll tax breaks, Loan Guarantees, Federal Reserve Credit Facilities. The legislation’s important impact on payroll: if you claim PPP benefits you do not get the employee retention credit.

Employee retention tax credit: $50 billion to companies that retain employees on payroll and cover 50% of worker’s paychecks.

To qualify, business must prove a 50% loss compared to the same quarter last year. Refundable credit against employer’s share of SS taxes, capped at 10k per employee

- Delay of Payment of Employer Payroll Taxes

- This would allow deferment of the 6.2% Social Security payroll tax.

- 50% due 12/31/21 and 50% due 12/31/22

How do you get these benefits?

Tenants and clients should talk to their accountants and legal team to find an SBA lender to fit their specific business type and needs.

https://www.uschamber.com/co/start/strategy/applying-for-sba-disaster-relief-loan

Economic Injury Disaster Loan (EIDL) Program: ONLY EIDL (Disaster loans) can be applied for online. Apply here: https://covid19relief.sba.gov/#/

How to Apply for PPP loan: application can be found here: https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Application-3-30-2020-v3.pdf

- Apply directly through an SBA approved lender

- Loan forgiveness- ONLY APPLICABLE TO PPP LOAN

Where do I go to apply?

Where are the qualified lenders? Find out here: US Treasury Link

Lenders authorized to make loans under the SBA’s current Business Loan Program are automatically approved to make and approve PPP Loans

- SBA qualified lender

- Can search for SBA lenders on SBA website

- Guidance, when issued, will list non-traditional lenders who can give SBA loans

- Need to go to a bank or a lender that has been authorized to give the loan under the CARES Act.

- If you have an existing SBA loan, or work with an SBA approved bank, start there.

Any other details I should know?

You can be considered for a $10,000 advance on your EIDL loan. Businesses who request this $10,000 advance on their loan and are approved are expected to receive it within three days. This $10,000 advance does not need to be paid back — though the rest of your disaster assistance loan will need to be paid back.

Borrow the max for PPP loans, no prepayment penalties.

No filing/closing fees from lender

PPP Loan- can still apply if you have already laid off employees, however the employees have to return by the end of June 2020.

Expanded Unemployment

- Most restrictions on eligibility suspended if related to COVID-19

- Additional $600 per week on top of regular state benefit (through July 31)

- Eligibility ends when individual can return to work

I need some tips keeping my business afloat during this time!

https://www.labor.ny.gov/ui/employerinfo/shared-work-program.shtm

NYS Department of Labor Shared Work – this could provide an alternative to laying off employees during business downturns by allowing workers to work a reduced work schedule and collect partial unemployment insurance benefits for up to 26 weeks

Clear definitions on essential workforce, https://esd.ny.gov/guidance-executive-order-2026 information for those NOT covered by the guidance in how to see a waiver

More helpful graphics: Located here, from the US Chamber